Signal Over Noise: Why Quantitative Models Explode in Low-Liquidity Equities

A mathematical defense of a curated workspace. This article details why Gammatic systematically excludes small-caps and penny stocks to eliminate model drift, focusing exclusively on high-liquidity index components where systematic flows are highly predictable.

Data

Executive Summary

Machine learning models are entirely dependent on data integrity. When a quantitative predictive engine is exposed to low-liquidity, highly fragmented equity environments, model drift occurs, resulting in catastrophic false-positive signals. This brief establishes the mathematical parameters of Gammatic’s restricted asset universe, explaining why restricting our data pipelines to highly liquid index complexes (SPY, QQQ, IWM) is an operational necessity for serious institutional operators.

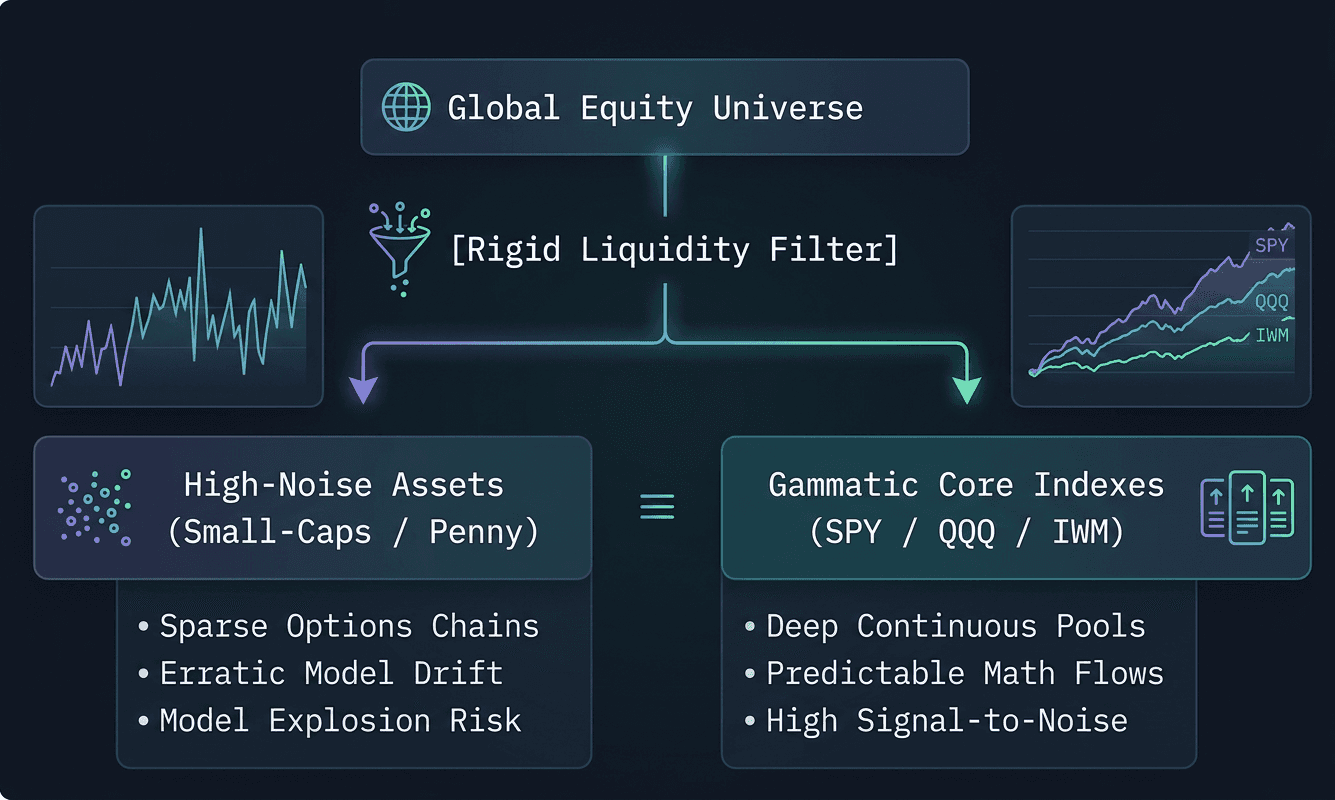

The Entropy of Fragmented Micro-Cap Liquidity

A common mistake among retail algorithmic traders is attempting to deploy advanced predictive models across thousands of micro-cap equities or illiquid small-cap stocks. The allure is obvious: these assets exhibit massive daily percentage swings that look highly lucrative on a surface-level scan. However, from a data science perspective, these environments are governed by pure entropy.

In low-liquidity equities, the options chain is sparse, open interest is highly fragmented, and the bid-ask spreads are wide. Because there is minimal institutional market-maker involvement, the structural physics that drive large-cap markets—such as dealer gamma hedging, vanna expansion, and systematic rebalancing—do not exist. A single retail order or a small block trade from a minor fund can completely distort the price action, creating massive data anomalies. If a machine learning model attempts to process this noise, it identifies false patterns, leading to severe model drift and rapid capital destruction.

Structural Predictability in Broad Index Architectures

Gammatic eliminates this structural vulnerability at the data ingestion layer by enforcing a rigid, non-negotiable asset boundary. Our network completely discards the noise of the broader market to focus exclusively on the core engines of global institutional liquidity: SPY (S&P 500), QQQ (NASDAQ-100), and IWM (Russell 2000) options surfaces.

These index complexes represent the deepest, most liquid continuous pools of capital on earth. Because they are the primary vehicles for programmatic hedging, macro index arbitrage, and institutional volatility trading, their options surfaces are continuous and highly efficient. The flows passing through these option chains are driven by cold, systematic mathematical rules rather than random human emotion. This creates an exceptionally high Signal-to-Noise Ratio, providing our XGBoost and Hidden Markov Models with pristine, predictable data streams.

Preserving Model Integrity via a Curated Universe

By intentionally restricting the terminal workspace to these liquid environments, Gammatic ensures that our predictive matrices operate at peak mathematical precision. Over an extended sample size of executions, the models maintain an institutional-grade predictive edge because they are calculating the actual mechanical requirements of institutional dealers.

For the serious operator, this curation is a massive structural asset. It completely eliminates the time wasted scanning thousands of worthless charts, focusing your analytical workspace entirely on the deepest liquidity pools where the math is reliable, execution fills are immediate, and capital can be scaled safely without moving the market.