Deconstructing Market Regimes: How Hidden Markov Models Isolate Systemic Tail Risk

An institutional-grade analysis of how Gammatic deploys Hidden Markov Models (HMM) to classify latent volatility states, filtering out structural noise and identifying systemic risk parameters before capital is ever deployed.

Research

Executive Summary

Conventional technical analysis operates on the flawed assumption that market volatility is continuous and linear. In practice, financial markets undergo sharp, non-linear structural phase shifts. This brief outlines how Gammatic implements a decoupled Hidden Markov Model (HMM) processing layer to programmatically classify latent regime states—ensuring operators position options capital with the statistical wind at their back, rather than fighting invisible structural tides.

The Latency of Conventional Risk Filters

Most retail platforms instruct traders to evaluate market risk using simple, trailing calculations like a 200-day moving average or standard Bollinger Bands. These metrics suffer from severe mathematical latency. By the time a moving average slopes downward, an institutional liquidity cascade has already occurred, and option premiums have already priced in the panic via explosive implied volatility expansion.

During systemic market shocks, asset correlations rapidly snap toward 1.0, rendering standard diversification strategies useless. Linear indicators fail because they treat every market environment as a single, uniform distribution. To preserve capital, an elite systematic framework must differentiate between a normal, mean-reverting pullback and a systemic regime shift before the price action completely breaks down.

The Mathematical Framework of Hidden Markov Layers

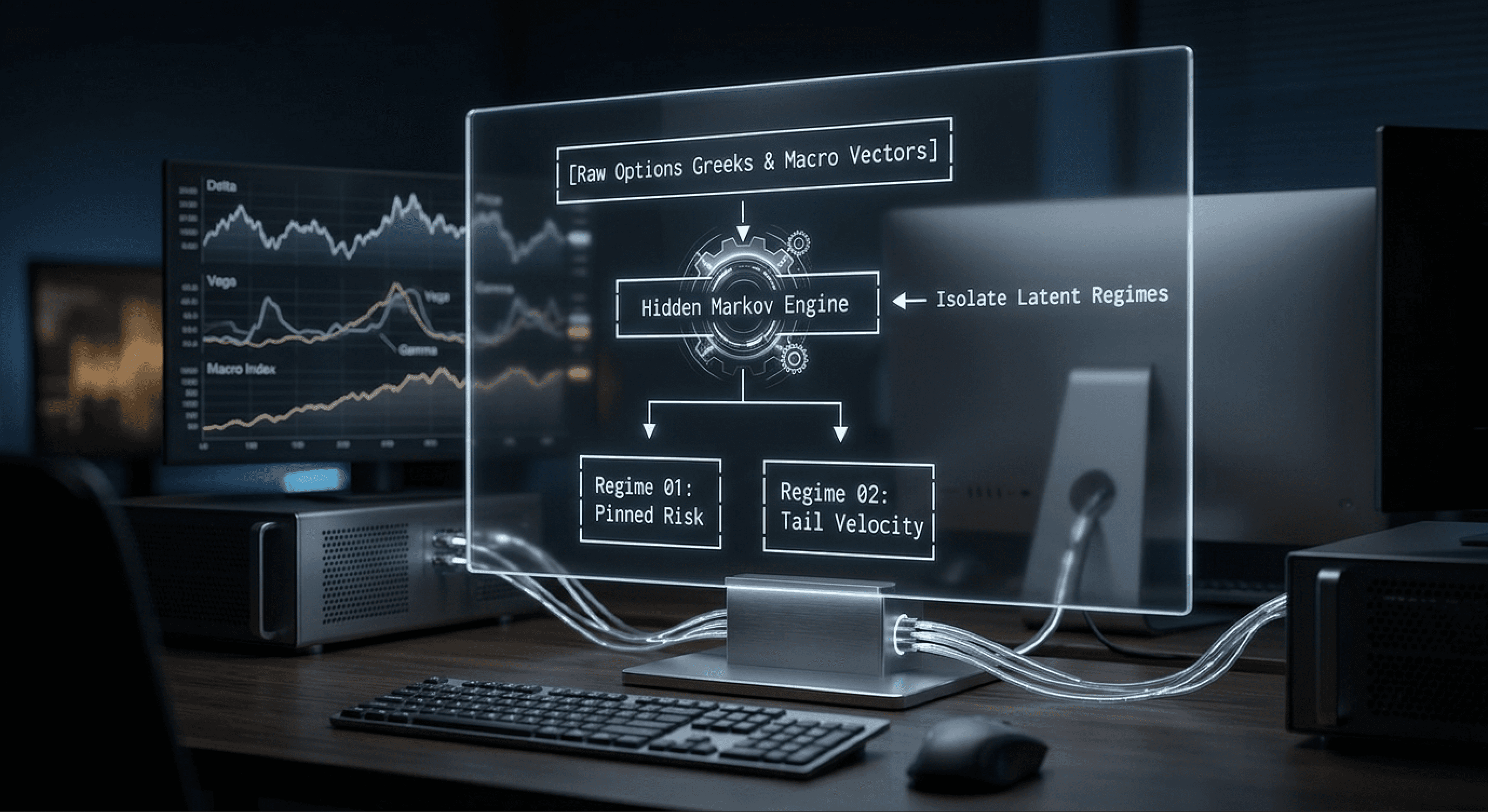

To solve this latency dilemma, the Gammatic network discards trailing geometric chart patterns and implements a decoupled statistical processing layer powered by a multi-state Hidden Markov Model (HMM).

An HMM operates on the premise that the true state of the market environment is "hidden" and cannot be observed directly through price action alone. However, by continually feeding the algorithm raw structural inputs—such as changing options implied volatility surfaces, overnight dealer delta allocations, and index kinematic vectors—the engine can reverse-engineer the probability of the current regime state.

The engine continuously classifies the market architecture into distinct, un-reconstructed mathematical regimes:

Regime 01 (Equilibrium / Compression): Volatility is strictly mean-reverting, institutional dealer gamma acts as a stabilizing cushion, and options premium decay curves are highly predictable. Under this regime, premium collection strategies possess a massive statistical edge.

Regime 02 (Expansion / Tail Velocity): Volatility vectors accelerate non-linearly, dealer hedging feedback loops turn reflexive (forcing market makers to short underlying equities into falling markets), and directional variance expands. Under this regime, standard delta-neutral strategies risk catastrophic tail-loss.

Terminal Execution: The Strategic Risk Filter

In the Gammatic ecosystem, this machine learning framework functions as your primary operational safety valve. Rather than generating random buy and sell alerts, the classified Markov state is piped directly into the Market Pulse control panel as a foundational condition.

Before an operator deploys a multi-leg options structure inside the Trade Designer, the terminal cross-references the active regime classification. If the Markov engine logs an active shift into an unpinned, high-velocity regime, the system updates your tactical parameters—allowing you to scale down position sizing, adjust volatility exposure, or completely halt execution before an institutional liquidation wave catches your portfolio exposed.